Google now has 9 apps with over a billion users

Google now has 9 apps with over a billion users

Alphabet’s billion user club and Android’s platform control

In addition to its central cash cow Google Search, Alphabet has built eight other software products with >1 billion users each:

Google Photos: >1.0 bn users

Google Maps – partially acquired in 2004: >1.0 bn users (MAUs)

Gmail: >1.8 bn users (DAUs)

YouTube – acquired in 2006: >2.0 bn users (MAUs)

Google Play Store: >2.5 bn users (MAUs)

Android – acquired in 2005: >2.8 bn users (MAUs)

Google Workspace: >3.0 bn users

Chrome Browser: >3.3 bn users

Several of Alphabet's most successful apps come from acquisitions. To date, >250 acquisitions have been carried out for a total consideration of $30 bn (most recently, cybersecurity firm Mandiant for $5.4 bn). Android was acquired in 2005 for a financially insignificant amount of $50m, but it's one of the smartest M&A deals of all time. In conjunction with Chrome, Android enables direct influence on important access points to the Internet and cements Search's market position on mobile.

Mobile operating systems can be described as a duopoly. Android reaches 72% market share, Apple iOS 27%. In emerging markets – where Android devices are available starting at $50 versus ~$400 for the cheapest iPhone – the situation is even clearer. Unlike the closed iOS, Android is an open-source project, whose source code can be downloaded, modified and used commercially for free. Alphabet aims to have the largest possible Android user base and later monetizes the OS indirectly through more searches and paid clicks. Theoretically, OEMs are allowed to sell mobile devices without Search or any other Google service. Amazon did this in 2014 with the Fire Phone based on Fire OS, a forked version of Android without Google apps. In practice, however, Alphabet tries to ensure the distribution of Search on almost all Android devices through contracts like the AFA, MADA or RSA. MADA requires device makers to pre-install all of the following Google apps if only one of them is supposed to come pre-installed on the device: 1) Search, 2) Chrome Browser, 3) YouTube, 4) Gmail, 5) Google Maps and 6 ) Google Play Store. The crux of the matter? Android users are able to install all of these apps themselves with just one click – except for the Play Store!

The Play Store is the exclusive access point to download software on Android devices. If it is not pre-installed upon delivery, it is practically impossible to download elsewhere. As a result, the device loses its appeal. In addition, software developers usually only develop apps for those app stores that have the most users (Apple and Play). Alternatives like MiMarket or Amazon's Appstore with <1% market share don’t justify any extra effort. One reason for the flop of the Fire Phone was its app store, which wasn’t competitive offering 200,000 apps at launch time compared to >1 million in Google’s Play Store. Because of this, all major manufacturers opt to sign the MADA, which qualifies them for an RSA in the next step. If they ship Google as the pre-installed default search engine, they receive a percentage of all advertising revenue generated through their devices in return. In 2021, I believe Alphabet paid $24 bn to its search distribution partners (of which ~$15 bn to Apple), or 16% of all Google Search & other ad revenues. From the OEM’s point of view, the RSA transforms a mobile operating system from a horrendous cost center if developed in-house to a direct profit center (for Apple, the ~$15 bn is virtually all profit). Android thus offers OEMs a convincing value proposition and is rolling out its software offering to future search platforms such as connected TVs, wearables or cars.

The rise of YouTube and the upcoming CTV era

Another successful acquisition – and unlike Android, a direct revenue contributor – is YouTube. Founded in 2005 by three former PayPal employees, YouTube has become the world’s largest video platform and now accounts for 20% of global mobile traffic. Before strong network effects between viewers, creators and advertisers came to fruition, the founders had to overcome the so-called "cold start problem". To do so, they uploaded videos to the platform themselves and asked friends and family to join in. Nevertheless, the video library did not show any growth for the first three months and by mid-2005, only 50 videos were available on YouTube. However, after a software update and simplified embedding of videos on Myspace, both the upload and download behavior picked up steam. By the end of 2005, thousands of videos had been uploaded and by mid-2006, over 100 million. One big problem at the time? Uploaded videos often contained copyrighted material, and the founders didn't have a sophisticated plan for dealing with a looming wave of lawsuits. Entrepreneur and investor Mark Cuban therefore painted a bleak picture for YouTube’s future at the end of September 2006:

„They are just breaking the law. There is a reason they haven’t yet gone public, they haven’t sold. It’s because they are going to be toasted. Anyone who buys YouTube is a moron. […] User-generated content is not going away. But do you want your advertising dollars spent on a video of Aunt Jenny watching her niece tap dance?”

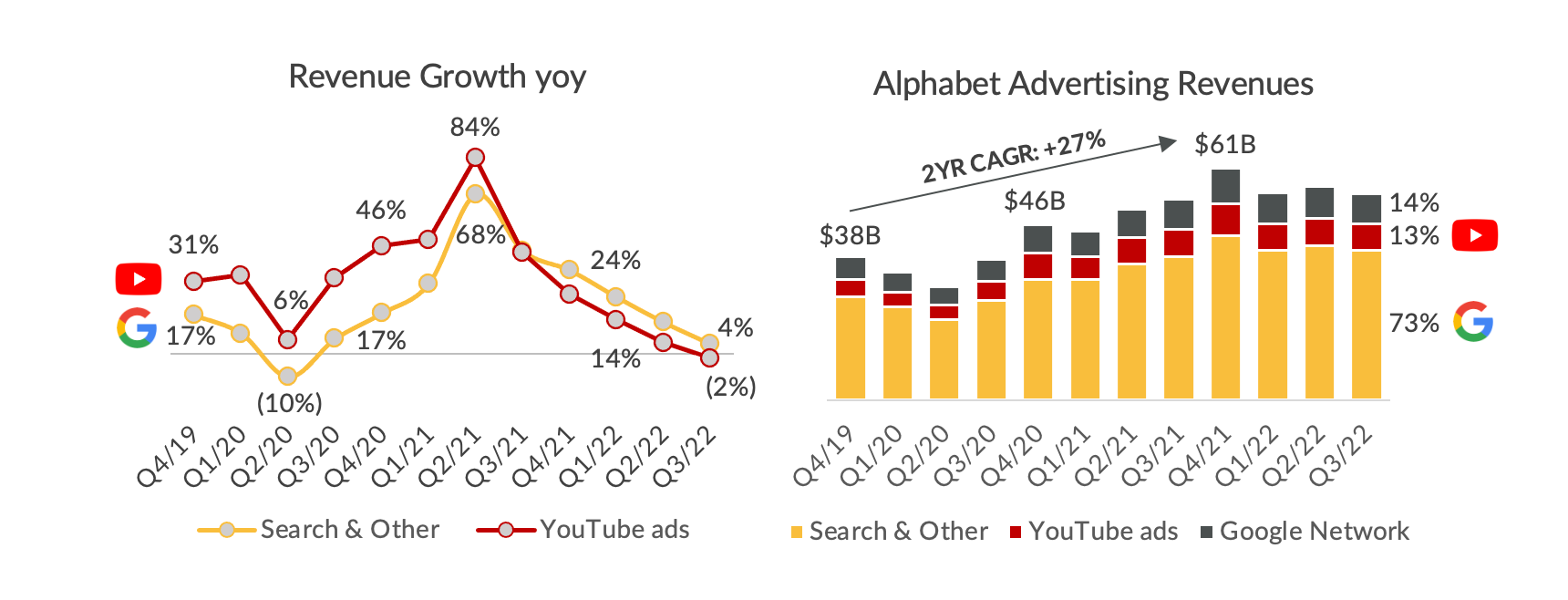

Exactly one week later, "moron" Google entered the stage and bought YouTube for $1.7 bn. The wave of lawsuits indeed came crashing down on the company, but in the most important case – Viacom International Inc. v. YouTube, Inc. – the parties settled out of court years later. In general, rightsholders were promised a revenue share and YouTube introduced video ads in connection with its YouTube-Partner-Program (YPP) in 2007. Large TV networks as well as smaller creators with more than 1,000 subscribers can participate in the YPP. YPP creators receive 55% of the advertising revenue generated in connection with their videos and YouTube gets the remaining 45%. The rest is history. By fiscal 2021, YouTube grew its advertising business to $28.8 bn and in terms of revenue is now recouping its heavily criticized $1.7 bn price tag every 3 weeks. For a long time, YouTube’s monetization was not pushed aggressively, but at the latest since the pandemic, the time of restraint is over (see graphs below).

YouTube has to be considered a COVID winner. More video consumption at home combined with an aggressively increased ad load enabled the platform to grow faster than Search until the end of 2021. YouTube stands for brand marketing, Search for performance marketing. During recessions, brand marketing is scaled back earlier and more significantly than performance marketing. That's why we're currently witnessing the trend reversal shown above with Search continuing a moderate growth trajectory while YouTube's ad revenue is shrinking for the first time in history. Over the long run though, I believe the video platform still has good opportunities to increase its advertising revenues thanks to three drivers:

…

The full PDF is available online here* (*by clicking the link, you confirm your status as a QUALIFIED INVESTOR) and QUALIFIED INVESTORS resident or domiciled in Germany can subscribe for full articles here.

This document is for informational purposes only. It is no investment advice and no financial analysis. The Imprint applies.