United States v. Live Nation-Ticketmaster

Some initial observations regarding the DOJ's most recent lawsuit

Last Thursday, on May 23, the DOJ and 30 states sued Live Nation-Ticketmaster for monopolizing several markets across the live concert industry through exclusive contracts in primary ticketing, threats, retaliation and illegal acquisitions of rivals.

As you know, I’m following United States v. Google LLC (2020) closely due to the fund’s investment in Alphabet and last month, I shared a detailed breakdown of what I think should happen next.

I’m not an investor in Live Nation-Ticketmaster nor any other concert promoter or ticketing company and therefore I’m no expert on the inner workings of the industry. Nonetheless, the 128 pp. strong complaint U.S. and Plaintiff States v. Live Nation Entertainment, Inc and Ticketmaster L.L.C. happened to be my weekend reading and I share some of my initial observations below.

Company Background

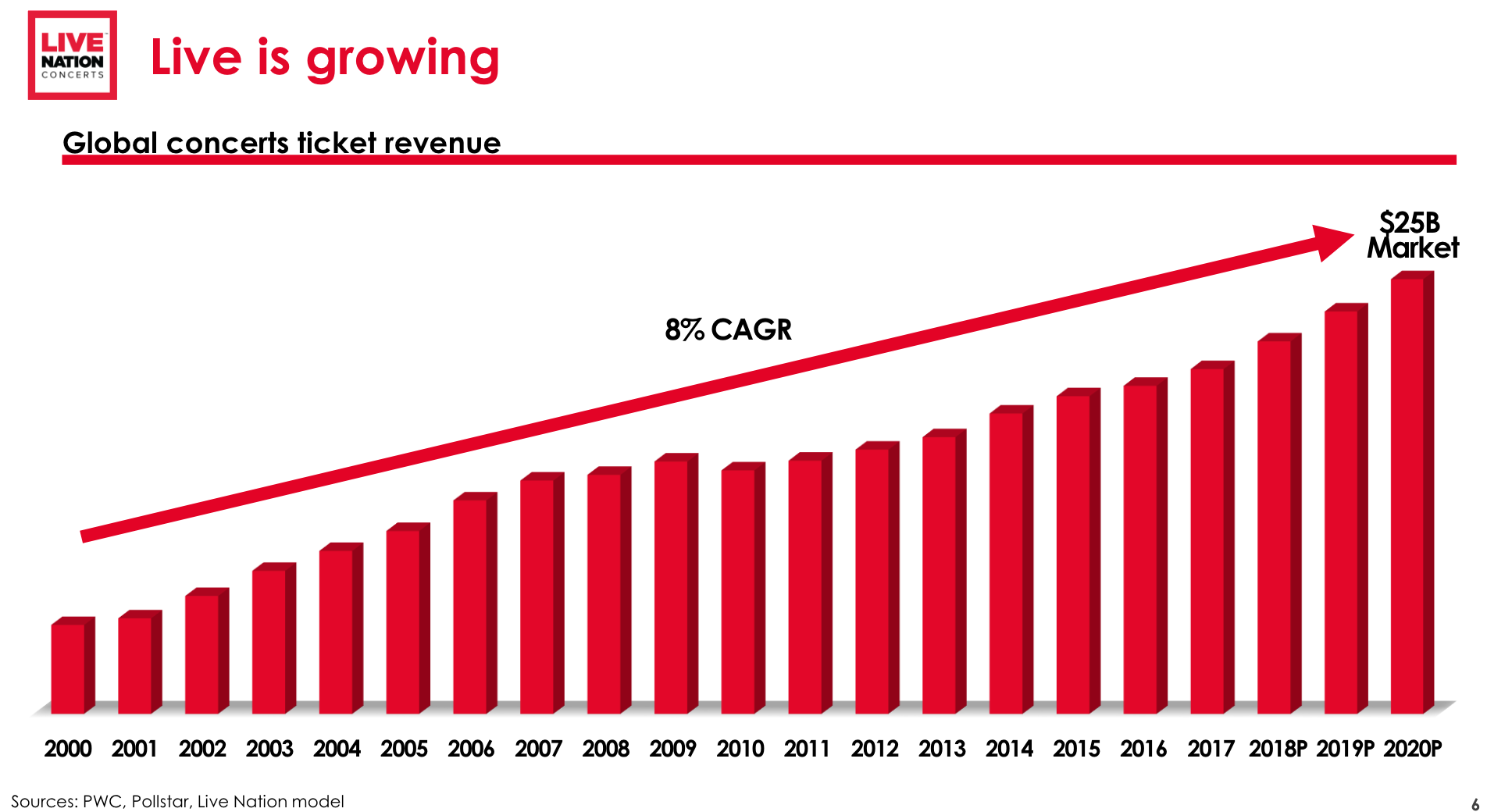

Live Nation Entertainment Inc. is the largest live entertainment company in the world and the largest producer of live music concerts. The company owns, operates or controls 373 venues globally (thereof 265 in North America, including 60 of the top 100 amphitheaters). It promoted 50,000 events from 6,800 artists in 2023, which means there is a Live Nation concert somewhere in the world every 10 minutes. Historically, live concerts has been a growth industry with a +8% CAGR in ticket revenue.

In a controversial 2009 merger, Live Nation joined forces with Ticketmaster, the market leader in primary ticketing services, followed by Live Nation as the #2 at the time. Last year, Ticketmaster distributed a total of 620 million tickets through its website www.ticketmaster.com, its app and other retail outlets.

Alleging the merger would likely substantially lessen competition, the DOJ and nineteen states challenged it under Section 7 of the Clayton Act but ultimately entered a consent decree as a final judgement in 2010. The decree was amended in 2019 and allowed the merger to proceed subject to the following conditions:

Live Nation and Ticketmaster are prohibited from creating mandatory bundles of their services and may not require that a client books Live Nation as a promoter in order to access Ticketmaster's primary ticketing services, or vice versa

Live Nation may not threaten to withhold concerts from a venue or retaliate against a venue if the venue chooses a ticketing service other than Ticketmaster

Live Nation must employ an internal antitrust compliance officer and the DOJ appointed an independent monitor to investigate the company’s compliance

Since 2020, the DOJ proclaims the consent decree has utterly failed to restrain Live Nation and Ticketmaster from violating other antitrust laws in increasingly serious ways. Therefore, the agency decided to move ahead and sue the company, seeking a divestiture of Ticketmaster at minimum. Live Nation’s share price declined 8% on the news.

Business Model

Live Nation has a $22 bn Enterprise Value and the company generated revenues of $23 bn in 2023, with $1.1 bn in EBIT (5% margin) on a total asset base of $19 bn with past ROIC averaging midteens (incl. goodwill) and mid-20s (excl. goodwill).

It operates three segments (Concerts, Ticketing and Sponsorship & Advertising) which show a large variation in profitability (see slide below from 2018).

I’ll now discuss the three segments briefly, before introducing Live Nation’s flywheel:

Concerts (82% of 2023 revenue, -4% of EBIT, 2% adj. operating margin): In the Concerts segment, Live Nation acts as a producer and promoter of music events and tours. An artist who plans a new tour will work with a promoter (either directly but more likely through his/her booking agent). The promoter then organizes the tour plan, secures appropriately sized venues, arranges for local production services and markets the show so that enough fans show up.

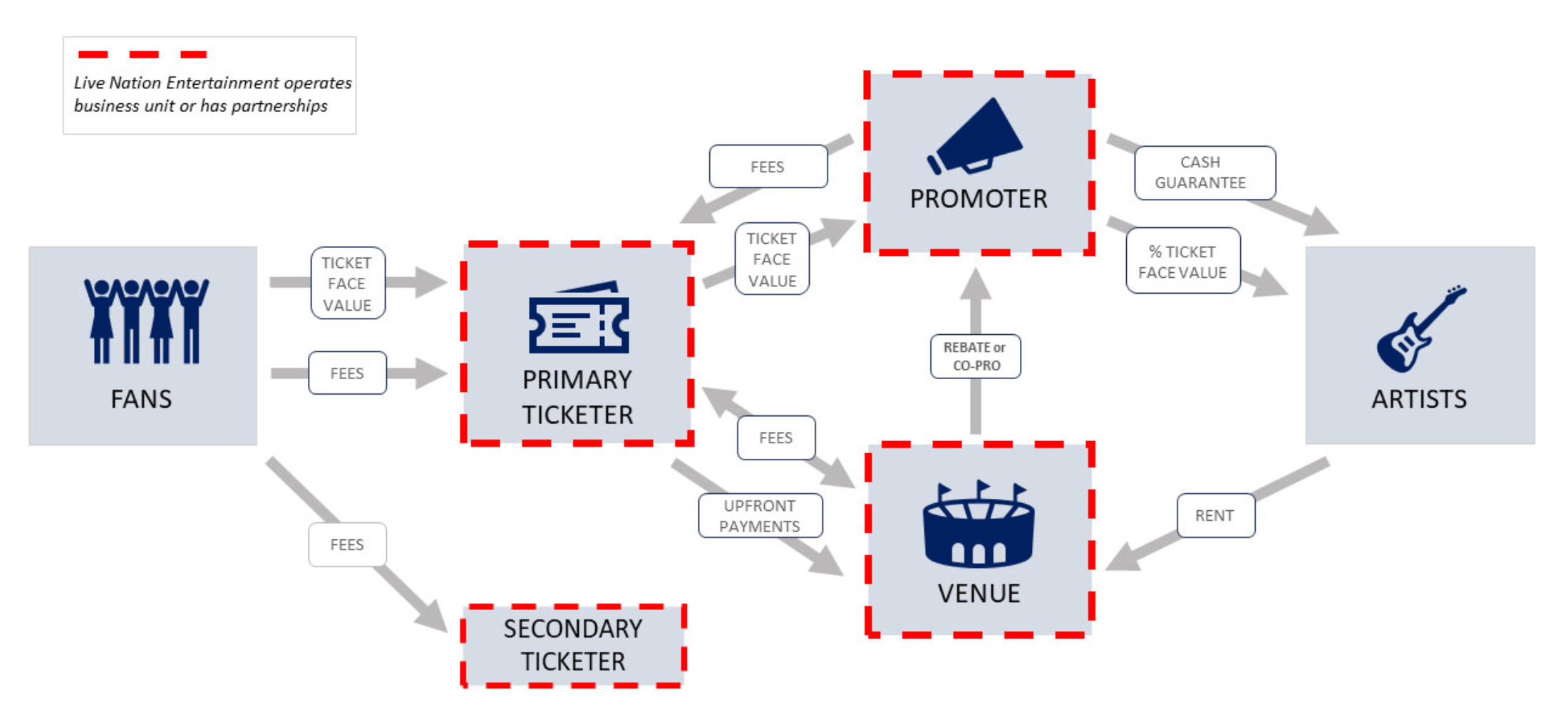

Whenever Live Nation acts as a promoter, the company earns revenues based on the value of total tickets sold. Let’s assume the face value of a ticket is $100 and added fees are $30, so a fan must pay $130 in total (as illustrated below). In step 1, the primary ticketing company (e.g. Ticketmaster) takes a 5% cut ($7 in the example) and pays a service fee to the venue. In step 2, the remaining amount flows to the promoter who must reimburse the artist and all remaining parties involved in the production of the show based on a pre-defined revenue split in step 3. Promoters may also receive payments directly from venues as an incentive to route popular artists to their venue. Ticketers like Ticketmaster often pay large upfront advances to venues in exchange for the exclusive right to sell their tickets.

The performing artist gets paid by the promoter under one of several different formulas, which may include fixed guarantees and/or a percentage of ticket sales or event profits. The artist pays rental income to the venue, calculated as a fixed fee and/or percentage of ticket sales. In practice, these rent payments often seem to be facilitated by and shared with the promoter. Minimum guarantees to artists from the promoter constitute the vast majority of their total income and, due to their fixed nature, promoters assume the risks of unprofitable events which they then try to mitigate through entering into national tour agreements where they can offset lower performing shows against higher performing ones.

In sum, Live Nation’s largest segment is a pass-through business, where 90%+ of the face value received from the ticketer is passed through to artists or spent on show production costs plus marketing. Live Nation operates the Concerts segment around Break-Even but its ownership of hundreds of venues and of Ticketmaster allows it to earn ancillary high-margin revenue streams, so that the firm can double-dip into the total value pie from ticket sales.

Ticketing (13% of 2023 revenue, 63% of EBIT, 38% adj. operating margin): Live Nation’s Ticketing segment contains its Ticketmaster business which carries significantly less direct operating costs than the Concerts segment (basically some call center costs and card fees). Ticketing therefore generates the majority of Live Nation’s profits (63% in 2023) and has a 38% adj. EBIT margin.

Sponsorship & Advertising (5% of 2023 revenue, 41% of EBIT, 62% adj. operating margin): Live Nation’s final segment is Sponsorship & Advertising where consumer brands choose to sponsor a concert/festival or pay for the right to have their name put on top of an arena. As you can imagine, these revenues carry no significant direct costs and generate a lofty 62% adj. EBIT margin.

Live Nation’s Flywheel

Live Nation began solely as a live events promoter in 1996 but over the following three decades integrated vertically into primary and secondary ticketing, venue ownership, music festivals, artist management and sponsorship & advertising. Below you can see how Live Nation increased its scope in the concert value chain (highlighted in red).

At the core of what Live Nation describes as its “flywheel” stands its role as a concert promoter which feeds into its ancillary high-margin revenue streams, i.e. ticketing and advertising. Live Nation’s CEO, Michael Rapino, once described it this way:

“At the core is our flywheel. It’s the concert business . . . It’s the lower margin part of our business. But in order to get into these three high margin businesses and be competitive, we have to have that scale [in concerts] . . . [Our] leadership position [in concerts] drives the three high margin businesses that are driving our true cash flow and EBITDA.”

In the U.S., the venues decide which ticketing service distributes their tickets. The face value of tickets are set or approved by the artists (in consultation with their manager and the promoter). Live Nation’s scale in terms of concert promotion (content) allows the company to exert meaningful influence on a) the venues to select Ticketmaster as their exclusive ticketer and b) on artists to work with Live Nation as their promoter, since they don’t want to miss out on the 373 venues the firm controls. Live Nation uses the alleged monopoly profits from ticketing and advertising to lock up artists to exclusive promotion deals, and then uses its clout in live content to sign venues into long term exclusive ticketing deals to ultimately fuel more high-margin ticket sales at Ticketmaster (see the flywheel below).

This self-reinforcing cycle lends itself to (mis)use an approach of “carrots” and “sticks” vis-à-vis venues and artists. Live Nation could threaten and retaliate against business partners who consider to work with a competitor. The DOJ proclaims the company has done just that and committed additional and more expansive violations of the antitrust laws compared to the narrower scope of the original Section 7 case from 2009. Therefore it decided to file a new lawsuit under Section 1 and 2 of the Sherman Act.

Legal Groundwork for the New DOJ Lawsuit

As I laid out in my latest Investor Letter, section 1 of the Sherman Act forbids “every contract, combination in the form of trust or otherwise, or conspiracy in restraint of trade” while section 2 of the Sherman Act forbids “monopolizing, attempts to monopolize or conspire to monopolize any part of trade or commerce”.

In plain English, section 1 of the Sherman Act forbids companies to form a cartel, divide markets or fix prices. These acts are per se violations of the Sherman Act. All other violations are analyzed under the rule of reason standard where a court examines the net result of pro- and anticompetitive effects of the challenged acts and if they unreasonably restrain trade.

Section 2 of the Sherman Act specifically targets monopolies and makes it illegal to acquire or maintain a monopoly through improper means. It’s important to note that having a monopoly due to a superior product or business acumen is perfectly legal and monopoly power will not be found unlawful unless accompanied by exclusionary or predatory practices!

Having read the complaint, I came away with the impression that the DOJ centers its case on five violations of the Sherman Act (two under section 1, three under section 2).

#1: The DOJ argues Live Nation has violated section 1 of the Sherman Act by unlawful exclusive dealing through entering into long-term exclusive ticketing contracts with venues which restrict the access of Ticketmaster’s competitors to the only significant channel of distribution for primary ticketing services.

#2: In another alleged violation of section 1 of the Sherman Act, the DOJ argues Live Nation has engaged in unlawful tying agreements by requiring artists seeking to use its large amphitheaters for shows to also purchase Live Nation’s promotion services.

#3: Regarding section 2 of the Sherman Act, the DOJ proclaims that Live Nation has unlawfully monopolized the market for the use of large amphitheaters through acquiring control over several amphitheaters, several competing concert promotion companies that either owned amphitheaters or had exclusive booking contracts with amphitheaters and acquiring several large festivals (e.g. Lollapalooza) as an alternative to Live Nation amphitheater tours.

#4: In another alleged violation of section 2 of the Sherman Act, the DOJ argues Live Nation has engaged in unlawful monopolization of the market for concert promotion services through acquiring rival promoters, accompanied by exclusionary conduct in the form of threatening potential entrants and their investors.

#5: Finally, as a result of the acquisition of Ticketmaster, the DOJ argues Live Nation has violated section 2 due to unlawfully maintaining its monopoly in the market for primary ticketing services through directly and indirectly threatening venues that Live Nation will divert live music shows to other venues if they do not sign with Ticketmaster.

Regarding #5, the DOJ seems especially concerned with collusion and division of business lines between Live Nation and the leading venue development and management company Oak View Group which controls a portfolio of 200+ U.S. venues. The agency proclaims both companies maintain a competitive standstill agreement under which OVG instructs its venues to use Ticketmaster as their primary ticketing service and refrains from competing against Live Nation in the concert promotion business as long as Live Nation brings sought-after events to OVG venues.

Potential Debates Around the Five Violations

In my opinion, debates around the alleged violations #1 to #5 could circle around the following questions:

#1: We know that exclusive dealing is often lawful. For the DOJ to prevail with its allegation that Ticketmaster’s exclusive ticketing contracts with venues are in breach of federal antitrust laws, it will need to show that the agreements foreclose at least 40% of the primary ticketing market to competitors and lead to reduced output or higher prices. Here, the DOJ will claim that Ticketmaster’s exclusive contracts cover more than 60% of all ticket sales to major concert venues and more than 75% of concert ticket sales to major concert venues and then try to build on an additional factor regarding the legality of exclusive dealing agreements, namely that the monopolist mustn’t threaten its contract partner. The DOJ will summon witnesses in court expecting to hear testimonies recounting plenty instances of direct threats and retaliation.

When it comes to Live Nation’s own venues exclusively contracting Ticketmaster, there is robust case law in my opinion that even a monopolist almost never has a duty to deal with one of his competitors (as established in Verizon Communications, Inc. v. Law Offices of Curtis V. Trinko with some rare exceptions, e.g. when there is a history of a prior profitable business relationship between two companies as established in Aspen Skiing Co. v. Aspen Highlands Skiing Corp.).

#2: Since tying is deemed unlawful only if 1) the seller has sufficient market power in the tying product and 2) can’t justify procompetitive benefits of his tying agreement, Live Nation’s legal counsel will most likely first question the DOJ’s market definition - the single most important question in any antitrust case - and then deny that the company possesses market power (legally defined as the ability to charge supra-competitive prices). It will lastly try to come up with procompetitive benefits of tying access to its amphitheaters to its event promotion business.

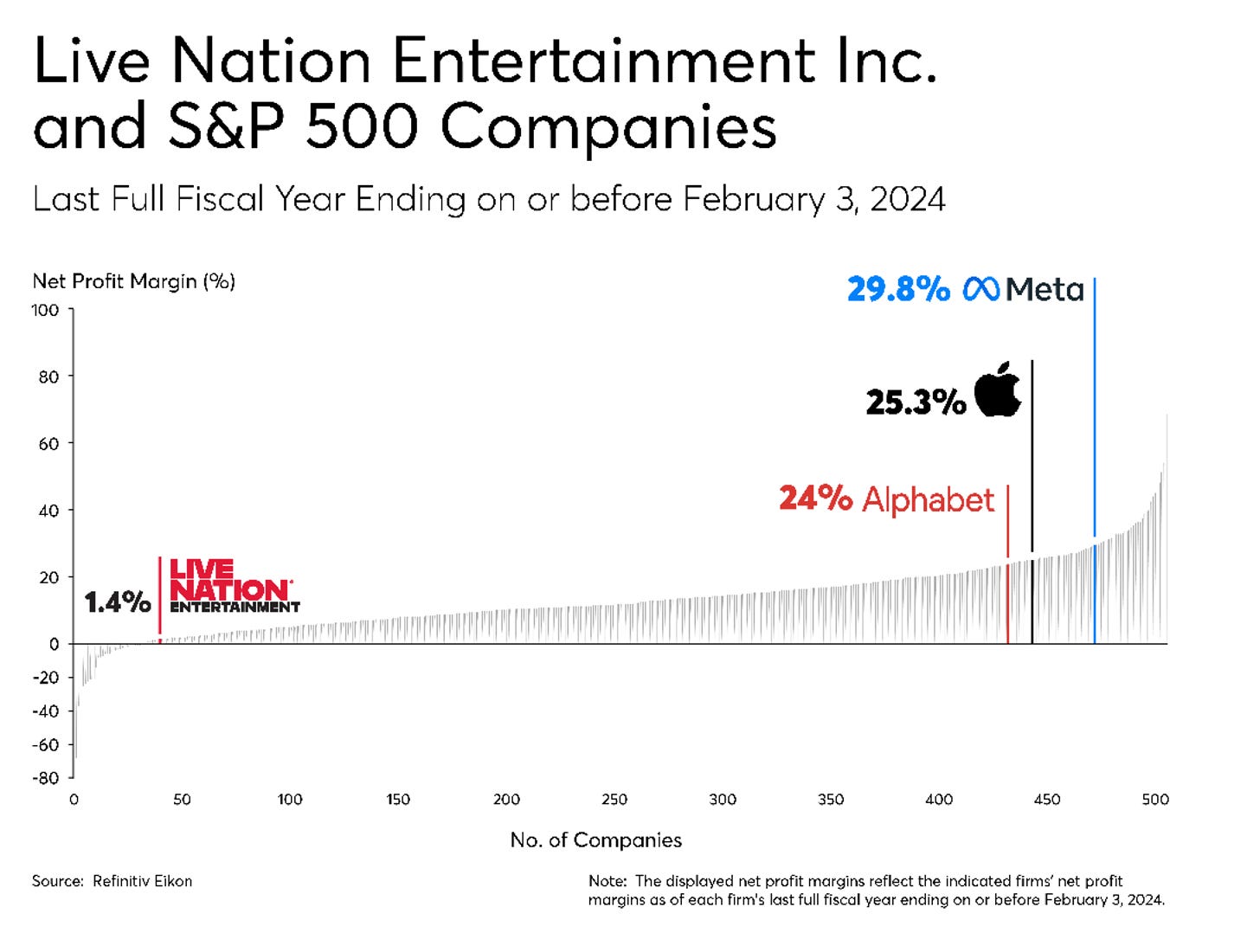

In a first rebuttal of the DOJ complaint, Live Nation’s head of corporate and regulatory affairs, Dan Wall, called it “absurd” that Live Nation and Ticketmaster wield monopoly power because:

“The defining feature of a monopolist is monopoly profits derived from monopoly pricing. Live Nation in no way fits the profile. Service charges on Ticketmaster are no higher than on SeatGeek, AXS, or other primary ticketing sites, and are frequently lower. In fact, when Ticketmaster loses a venue to SeatGeek, service charges usually go up substantially. And even accounting for sponsorship, an advertising business that helps keep ticket prices down, Live Nation’s overall net profit margin is at the low end of profitable S&P 500 companies.”

Concerning the DOJ’s remaining three alleged violations of section 2 of the Sherman Act #3, #4 and #5, the plaintiff identified three distinct markets that it deems Live Nation has unlawfully monopolized:

the market for the use of large amphitheaters

the market for concert promotion services and

the market for primary ticketing services

The DOJ alleges that Live Nation has monopoly power in each of those markets. As plaintiffs generally try to show monopoly power in court through indirect evidence in form of high market shares, the agency proclaims that Live Nation has the following market shares:

65%+ in the market for the use of large amphitheaters

60% in the market for concert promotion services and

70% in the market for primary tickets sold at large arenas and amphitheaters (80% in the subcategory of concert tickets sold at large venues excluding sports tickets)

Since the Supreme Court has never held that a party with less than 75% market share had monopoly power and lower courts generally require market shares between 70% and 80%, Live Nation’s lead litigators will try to refute the claims that Live Nation has monopoly power in markets 1. and 2.

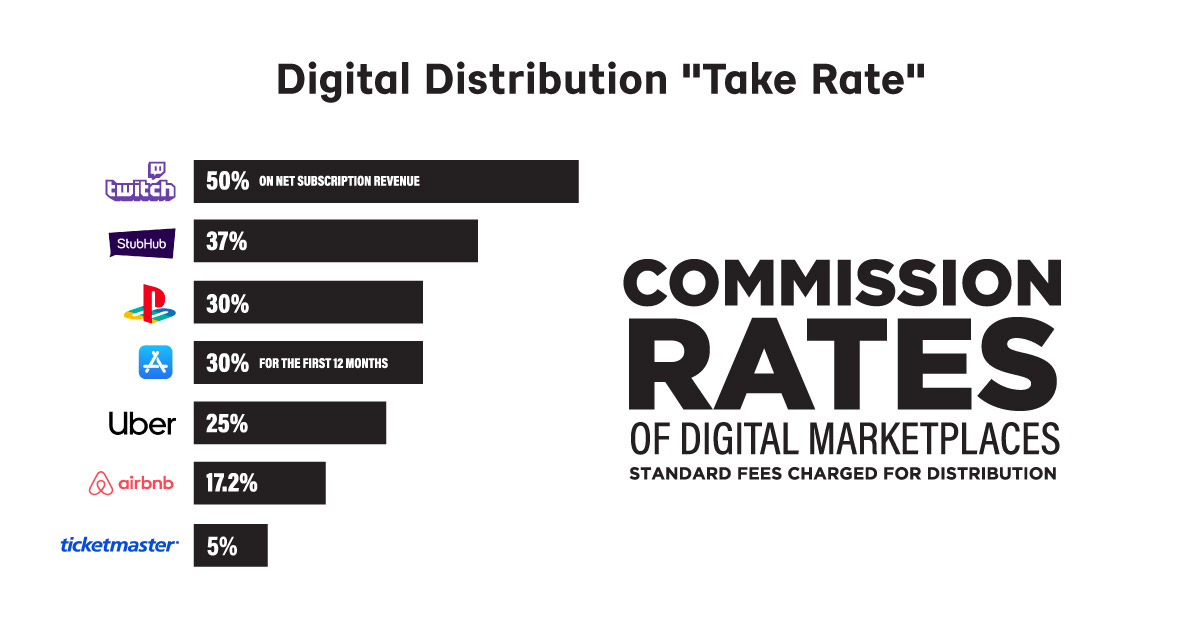

When it comes to market 3. for primary ticketing services, Live Nation will trace its leading position in this market back to its acquisition of Ticketmaster which the DOJ itself(!) signed off subject to the conditions from the consent decree. During trial, the defendant will resurface the agency’s own former argumentation that it could not prove that the merger would significantly harm competition. Additionally, Live Nation will try to show that SeatGeek and AXS have been gaining share and question the DOJ’s narrow market definition (only looking at concert tickets sold at large venues) because when including sports events and smaller venues, Ticketmaster sees its market share closer to 50% which is inadequate as a matter of law to constitute monopoly power. Finally, Live Nation will emphasize that its base take-rate in primary ticketing is rather low compared to other digital distribution channels.

In the now following final part of this post, I share with you the sections of the complaint which I found the most interesting before drawing a short conclusion.

Tidbits From the Complaint

p. 2: The DOJ’s most sought-after remedy seems to be the divestiture of Ticketmaster (at the least). Therefore, it opens its complaint making the argument that Live Nation wields monopoly power in the market for primary ticketing services.

p. 6: In court, it will be crucial for the DOJ to demonstrate consumer harm from Live Nation’s allegedly anticompetitive conduct. Therefore, the agency tries to frame the multiple fees added to the face value of tickets as a so-called “Ticketmaster Tax” that ultimately leads to higher prices for U.S. consumers compared to other countries.

p. 11: The next section explains what tasks a concert promoter fulfills when planning a tour. The two largest players are Live Nation and Anschutz Entertainment Group.

p. 13: The DOJ also tries to show that large amphitheaters are a distinct market.

p. 14: In the complaint, it is noted that almost all major concert venues contract exclusively with a primary ticketer.

p. 20: The face value of tickets is set or approved by artists but Ticketmaster has two dynamic pricing tools which allow face values to increase in case of surging demand.

p. 21: The service fee is regularly the highest fee added on top of the ticket’s face value to the annoyance of fans. The service fee gets passed from the ticketer to the venue but since Ticketmaster retains a portion of it, the venues decision of how high to set this fee doesn’t happen in a vacuum.

p. 25: Regarding the DOJ’s claim that Ticketmaster engages in unlawful exclusive dealing through entering into long-term exclusive ticketing contracts with venues where it retains the right to sell all of the venue’s primary tickets against an upfront payment, the DOJ will try to show that Ticketmaster coerced and threatened its venue partners. Live Nation has responded that it has never engaged in systematic threats and that since the independent Monitor was appointed almost 15 years ago “exactly one instance of potential concern has come to his attention. Otherwise, the Monitor has praised Live Nation for its compliance program and an exemplary record of compliance.”

p. 31: The DOJ made the following remarks regarding the alleged collusion and illegal dividing of business lines between Live Nation and Oak View Group, which Live Nation called “farcical” in its rebuttal.

p. 35: Live Nation allegedly threatened rival promoter TEG, backed by PE Silver Lake, through complaining to OVG executives, where Silver Lake also holds an ownership position. Live Nation retorted on May 23 that “there is no truth that this brief exchange had anything to do with Silver Lake’s decision to sell its stake in TEG”.

p. 48: The DOJ proclaims that Live Nation has engaged in multiple illegal acquisitions which sole purpose was to eliminate a competitor. In Utah, where regional ticketing company SmithsTix was outcompeting Ticketmaster, Live Nation considered to acquire the company. However, since the consent decree from 2010 made acquiring a horizontal ticketing competitor infeasible, Live Nation instead bought the leading venue operator in Utah, United Concerts, and flipped all its venues from SmithsTix to Ticketmaster after closing. SmithsTix subsequently went out of business.

p. 49: Live Nation acquired a regional promoter in the Southeast, AC Entertainment. It explicitly called the economics behind the deal “not super exciting” but still saw benefit in the acquisition due to the resulting “lower competition in the region”. Live Nation rejected the DOJ’s claim that this acquisition was objectionable in any kind since: “this was an acquisition of one promoter, who was in his 60s and looking to retire. He approached Live Nation looking to find a good, long-term home for his employees. Live Nation did not have a Knoxville office, so for $15 million it made the deal. Seriously? The DOJ is challenging that?”

Conclusion

The DOJ and 30 states seek a jury trial at the U.S. District Court for the Southern District of New York, which means everyday people will decide in first instance whether Live Nation broke federal antitrust law or not. The potential remedies will nonetheless be decided by a judge. The DOJ seeks a divestiture of Ticketmaster and a divestiture of owned or controlled venues is also possible, accompanied by an enjoinment on Live Nation from continuing its alleged anticompetitive conduct.

A jury trial is unusual but the DOJ may want to leverage the public’s discontent with Live Nation-Ticketmaster, especially after a botched ticket presale of Taylor Swift’s Eras tour two years ago, which made national headlines and even led to a congressional hearing. The DOJ reportedly opened its new investigation into Live Nation shortly after this incident (take-away: don’t mess with the Swifties!).

In an investor call regarding the lawsuit, Live Nation stated it wants to get the case to trial within a year and a half and it plans to get parts of the complaint dismissed in the next 60 days. I take no view on the outcome of the lawsuit, but two things seem clear: 1) a final verdict in the case is years away and 2) Ticketmaster as a spun-off company would be viable and valuable in its own right. The overarching insight however is a different one. With an imminent ruling in United States v. Google LLC (2020) and trials against Meta, Amazon and Apple waiting next in line, the topic of how investors plan to handle regulatory risk in the future will only grow more important.

[end of post]

If you don’t want to miss anything, you can follow me on Twitter: @patient_capital

To learn more about the investment fund I advise or access my previous annual letters to investors you can click the button below.

This document is for informational purposes only. It is no investment advice and no financial analysis. The Imprint applies.

fantastic overview, thank you Timo!